01

Term life insurance

Coverage for a set period, such as 10, 20, or 30 years. Typically the lowest initial premium. No cash value; if the term ends and the policy is not renewed or converted, coverage stops.

01 · Types of life insurance

Coverage for a set period, such as 10, 20, or 30 years. Typically the lowest initial premium. No cash value; if the term ends and the policy is not renewed or converted, coverage stops.

Permanent coverage with fixed premiums and a cash value component that builds over time on a schedule set by the policy.

Permanent coverage with flexible premiums and an adjustable death benefit. Cash value grows based on interest credited by the insurer.

Permanent coverage where cash value growth is linked to the performance of a market index, subject to caps and floors set by the policy. The cash value is not directly invested in the market.

02 · Term vs. permanent

Term insurance is like renting a home. You pay for protection while you need it, and the payment is lower. But when the lease ends, you walk away with nothing owned.

Permanent cash-value insurance is like buying. The payment is higher, but part of it builds equity: cash value you may be able to access later for goals of your own, while the coverage stays in place.

Like any analogy, this one simplifies. Which type fits depends on your budget, time horizon, and what you need the coverage to do. That is the conversation we have with you before recommending anything.

Life Insurance · The Life Capitalized Concept

The Life Capitalized Concept uses permanent cash-value life insurance as the foundation of a personal banking-style strategy, then pairs it with investment advisory to help pursue growth opportunities across your full financial picture.

Advisory services offered through Hornor, Townsend & Kent, LLC (HTK), Member FINRA/SIPC.

03 · The outcome

A personal pool of capital you can access on your terms, measured by policy cash value building alongside a coordinated investment plan, built by combining permanent cash-value life insurance with investment advisory aimed at your long-term growth goals.

Making financial decisions can be overwhelming. We simplify the process and walk you through how cash value and compound interest work together inside this strategy.

04 · The Life Capitalized Concept

The infinite banking concept uses a permanent cash-value life insurance policy as a personal financing system. As you fund the policy, cash value accumulates. You can borrow against that value for your own goals, while the underlying death benefit continues to protect the people who depend on you.

We select policies from established, well-managed insurance companies and structure them around your situation, then layer investment advisory on top so your broader portfolio is working toward the same goals.

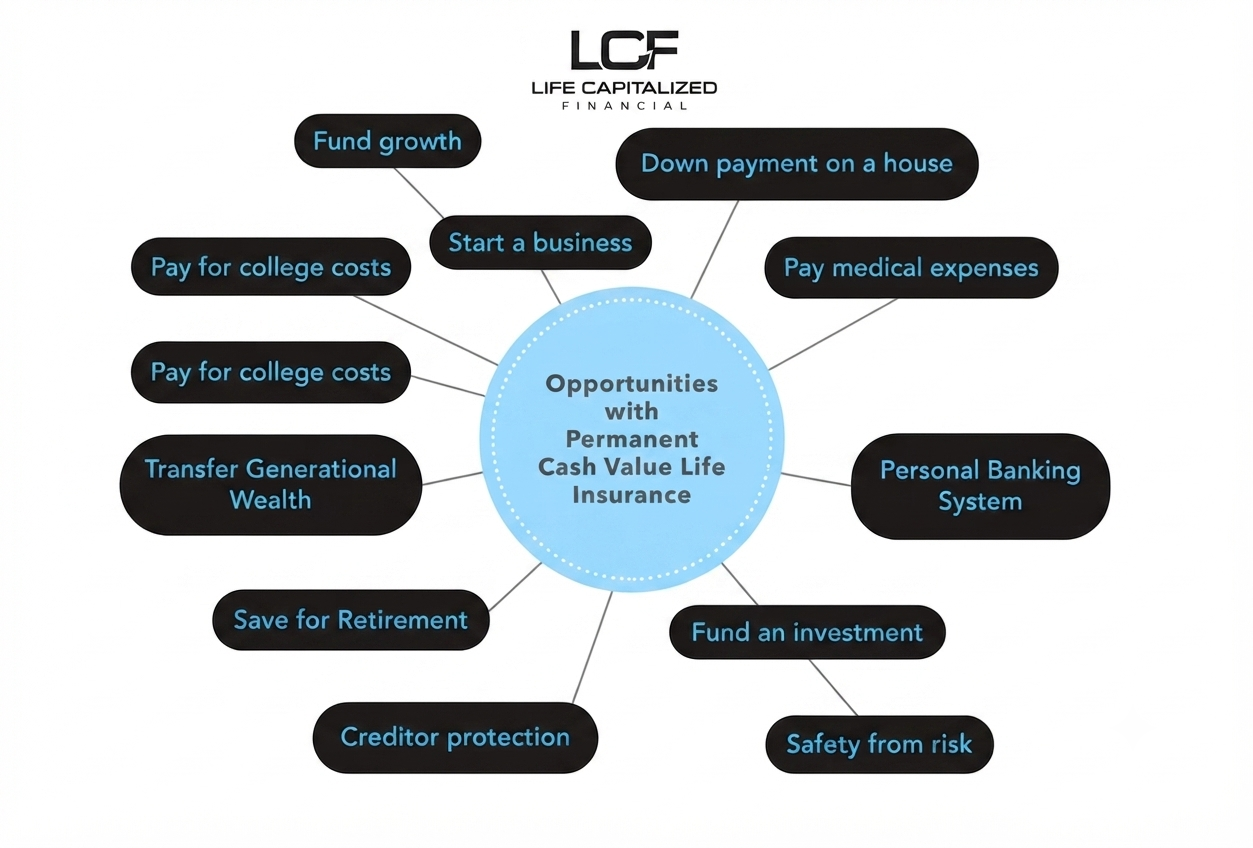

Learn how this fits your plan05 · Opportunities with permanent cash-value life insurance

Access is not automatic or unlimited — see the disclosure below on loans, withdrawals, and policy impact.

Tap accumulated cash value to help fund a new venture or fuel growth in an existing one.

Use policy cash value as one funding source alongside your broader education savings plan.

Access cash value to help with a down payment when the opportunity arises.

Draw on cash value to help cover unexpected medical costs.

Use your policy as a source of financing you control, in place of or alongside a traditional lender.

Access capital to act on an investment opportunity, coordinated with your advisory plan.

Use permanent life insurance as one part of a diversified approach to managing financial risk.

Depending on your state, cash value life insurance may carry certain creditor protections. Ask us about Florida's rules.

Build cash value as one leg of a retirement plan alongside your other accounts.

Pass a death benefit to the next generation as part of your estate strategy.

06 · Investment advisory, layered in

The Life Capitalized Concept does not stop at the policy. We add investment advisory to help you pursue growth across your full portfolio, coordinated with the cash-value strategy rather than running separately from it.

07 · Disclosure

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure you are insurable. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges; if a policy is surrendered prematurely, there may be surrender charges and income tax implications. You should consult a qualified tax professional for tax advice on your own personal situation. All guarantees are based upon the claims-paying ability of the issuer.

Accessing cash values may result in surrender fees and charges, may require additional premium payments to maintain coverage, and will reduce the death benefit and policy values. Loans are income tax free as long as the policy is not a "modified endowment contract" (MEC) and the policy must not be surrendered, lapsed, or otherwise terminated during the lifetime of the insured, and withdrawals must not exceed cost basis. Partial withdrawals during the first 15 policy years are subject to additional rules and may be taxable. Excess policy loans can result in termination of a policy. A policy that lapses or is surrendered can potentially result in tax consequences. You should consult a qualified tax professional for tax advice on your own personal situation. All guarantees are based upon the claims-paying ability of the issuer.

All investing is subject to risk, including the possible loss of the money you invest. No strategy assures a profit or protects against loss.